Large Ether Traders Position for Volatility Spike as Merge Draws Near

Taking unhedged or hedged directional bets on an asset's price is seen by some as the most exciting trading strategy in financial markets. And ether (ETH) traders have been doing exactly that ahead of the impending upgrade, known as the Merge, of the cryptocurrency's parent blockchain, Ethereum.

Institutions seems to be adopting an options trading strategy called a long strangle, which is indifferent to the direction in which the cryptocurrency moves and instead aims to make a profit from the degree of price turbulence or volatility.

"Block traders have also started betting on a volatility spike in ether," Griffin Ardern, a volatility trader from crypto asset management firm Blofin, said, drawing attention to large strangle trades that crossed the tape on dominant crypto options exchange Deribit in the past 24 hours.

A long strangle involves buying both call and put options with similar expiries. Buying a call – or the right to buy the underlying asset at a preset price – is akin to purchasing insurance against bullish moves by paying a premium upfront to whoever is selling the option. Buying a put – or the right to sell the asset at a predetermined price – is analogous to purchasing protection against price slides. Buying both protects against volatility.

The strategy makes money when the asset price swings enough in either direction to make the call or put more valuable than the total premium paid to purchase both options. The strategy bleeds money when the asset is little changed, reducing the demand for and prices of options.

According to Arden, the latest block – or large – trades signal increased interest in long ether strangles, pointing to confidence among sophisticated traders that volatility is set to explode.

The increased interest in volatility trading also points to market maturity and an influx of sophisticated traders into the industry. Block trades are large trades made by institutions that are generally broken into smaller orders and executed through different brokers or over the counter to ensure minimal impact on prices.

"They are willing to pay relatively higher costs to obtain possible high returns," Arden said.

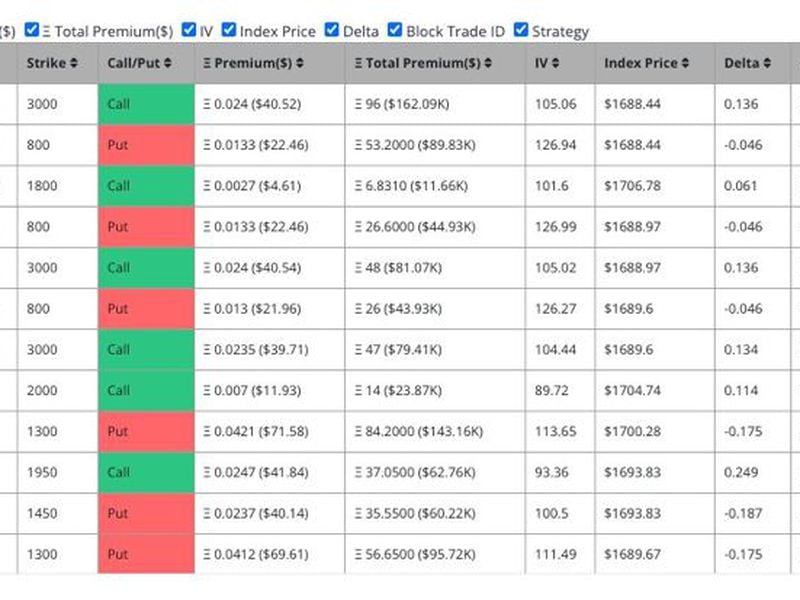

Block traders have set up strangles in options with Sept. 9, Sept. 30 and Oct. 28 expiries. Options expiring on Sept. 30 and Oct. 28 will capture both pre- and post-Merge market activity.

The first one in the table has the trader long 4,000 contracts at $3,000 strike call and long 4,000 contracts at $800 strike put, both expiring on Oct. 28.

The strategy will make money if ether settles well beyond the $800-$3,000 range on Oct. 28, making the call or put more valuable than the initial per contract cost of $62.98. That figure is reached by adding the premium paid for one call option contract, $40.52 and one put option contract, $22.46. The total premium paid for buying the 4,000 call and put contracts is $251,920. The calculation is based on figures mentioned in the above chart.

The entire premium paid will be lost if ether settles inside that range on Oct. 28, assuming the buyer holds the position until the settlement date. However, traders often liquidate positions before the expiry, depending on market conditions.

For example, suppose that before or immediately after the Merge there is a volatility explosion that's big enough to make either call or put more valuable than the total cost. In that case, the trader can liquidate positions and pocket the difference. If the Merge turns out to be a non-event, option prices will slide and the trader can cut back on losses by immediately squaring off the long strangle.

Its quite clear, volatility trading is complicated even though it looks easier than directional trading at first. It requires active management of positions and deep know-how of the so-called greeks – delta, gamma, theta, vega, and rho – factors that affect options prices.

That's why non-directional trading is best suited to sophisticated traders or institutions with ample supply of expertise and capital.

Related news

Celestia's TIA Braces for Price Volatility Amid $900M Token Unlock

Bitcoin Tops $73.5K, Climbing Just Shy of New Record High

Crypto Stocks MicroStrategy, Coinbase and Marathon Post Just Modest Gains as Bitcoin Eyes Record High

Bitcoin Miner HIVE Poised to Double Its Hashrate by Next Year, Cantor Says Initiating Stock at 'Overweight'

First Mover Americas: BTC Jumps Above $71K, DOGE Leads Market Surge