Crypto Long & Short: When Regulating Crypto, Please Target the Bad Actors, Not the Asset

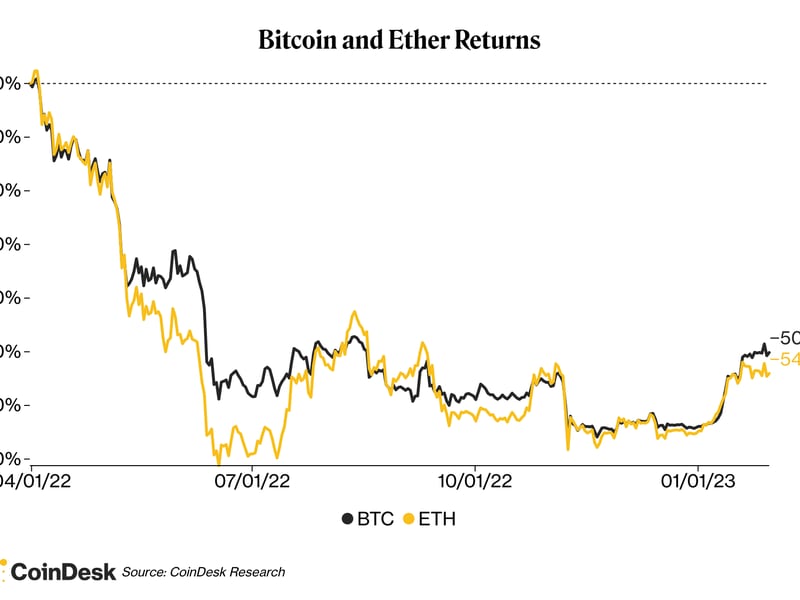

There’s no denying 2023 feels a lot better than 2022. Bitcoin (BTC) and ether (ETH) are up about 39% and 33%, respectively, so far this year, on the heels of 60% annual declines.

The U.S. Federal Reserve appears to be winning its inflation battle, improving the macroeconomic landscape and boosting investors’ appetite for riskier things like cryptocurrencies. Both BTC and ETH have price momentum and their trading volume is up, suggesting that bullish sentiment is increasing.

These two giants of crypto – together, BTC and ETH make up about 60% of total market capitalization of digital assets – are succeeding in ways that individual players have not. Do you need to be reminded of the troubles at FTX, Genesis, Gemini, Three Arrows Capital, Celsius ...?

The scandals and blowups of 2022 have set the scene for a regulatory and legislative crackdown in the months and years ahead. People who placed their hard-earned money into entities they trusted lost money – in some cases, years of savings disappeared. The resulting blowback and negative contagion impacted asset prices substantially, causing losses for people who simply owned certain cryptocurrencies. But this was not a problem with the crypto assets themselves. It was the actions of bad actors.

So where do we go from here? A couple things caught my eye this week. The first was the Jan. 27 “Roadmap to Mitigate Cryptocurrencies Risk” released by the Biden administration. The second was a Jan. 25 forum held by the American Economic Liberties Project, focused on confronting challenges within crypto.

Here are some quotes and ideas that stood out to me:

- ”Crypto fraud is a big problem.”

Agreed. Fraudulent activity within the crypto sector has stained the industry and had a significant negative impact on asset valuations. The resultant contagion has created additional uncertainty for nearly all parties involved with cryptocurrencies. I would argue that this is a sentiment shared by many within the sector.

- “While cryptocurrency might be relatively new, the behavior we have seen some cryptocurrencies exhibit, and the risks posed by this behavior, are not.”

Again, I don’t see a problem with this. In fact, it gets to the heart of one of my primary thoughts. The turmoil within the crypto sector was caused by individuals engaging in different variations of reckless behavior that has existed for decades. It wasn’t born out of crypto. These things happen outside crypto, too.

Greed and fraud are not isolated to cryptocurrencies, so it confuses me when part of the ire turns to the asset itself rather than towards the people committing fraudulent acts. If I were to be scammed out of U.S. dollars, my issue would be with the scammer, not the greenback.

- No one is using crypto as a currency.

This comes across to me as the “no one uses bitcoin to buy coffee” argument. Each time I hear this I raise an eyebrow. Sure, I haven’t come across many people willing to exchange bitcoin for a cup of coffee, though they very well may exist. (Yes, somebody did pay 10,000 BTC for pizza in 2010. Hope it was good.)

Yet, there are arguments bolstering the idea that bitcoin is 1) a store of value, 2) a unit of account and 3) a medium of exchange. Thus, I’d argue that bitcoin upholds the principles of a currency.

But bitcoin is also clearly a commodity. It’s been deemed one within the U.S. Commodity Exchange Act. I’d argue that commodities are purchased for the purpose of hedging risk and/or generating speculative profit. To that end, while it can be used for daily transactions, that’s not optimal. I wouldn’t use wheat or soybeans to purchase a cup of coffee either, but that doesn’t make those things pointless.

- Crypto is magic money to trade or buy drugs on the internet.

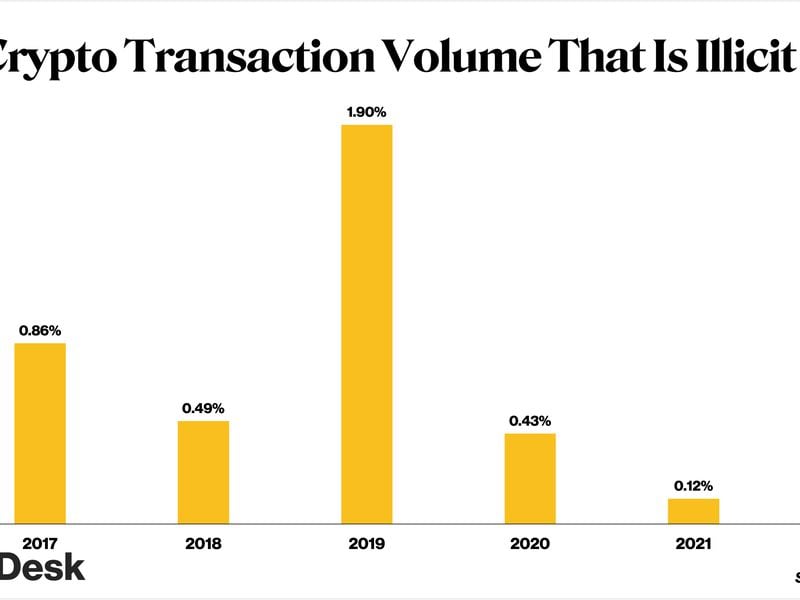

I see this as an extremely broad mischaracterization of the crypto community. (Also, I’d argue that anyone who thinks it's a good idea to purchase illegal narcotics via a publicly viewable blockchain is not thinking clearly.) In fairness to those worked up about this, there are ways to disguise illicit transactions, including through the use of privacy coins. Still, a recent Chainalysis report indicates that illicit activity accounts for only 0.24% of cryptocurrency transactions. This is an increase from 2022 and equates to an all-time high of $20 billion.

So, illegal transactions certainly occur via crypto, but I think more focus should be placed on the 99.76% of transactions that are not.

- Crypto is not for financial inclusion.

I disagree with this vehemently. People of color both inside and outside the U.S. are largely locked out of the benefits of asset ownership enabled by traditional finance. I believe part of their motivation to get exposure to crypto, whether via ownership or understanding, is to avoid being on the outside looking in. It’s an attempt to gain a foothold quickly before it becomes more challenging to do so, like it tends to be in traditional finance.

I’d submit that it's often implied that individuals within those communities simply don’t understand the risk involved. And I take issue with that. I would also argue that tremendous opportunity exists not just related to financial inclusion but bridging digital divides. I would welcome initiatives where underrepresented communities gain access to crypto both on the basis of asset ownership, as well as in learning about the technology underpinning it.

- Crypto is for speculation.

This is an odd criticism to me because I agree that crypto is used for speculation. I just don’t think there’s anything wrong with that. Any asset I purchase in financial markets is one that I would like to see increase in value. Sometimes the result goes my way … and sometimes it doesn’t. I think it's perfectly fine to engage in responsible speculation, with informed decision-making, the application of risk management and the expectation of profit and/or acceptance of loss.

- Crypto is all a scam.

I don’t see anything positive that can come from this characterization. By the same token, I don’t feel any need to change the minds of people who think this. If someone believes that crypto is a scam, I would 100% encourage them not to acquire it. For those who do believe in the asset, I would encourage them to buy it.

For institutional investors, a shift in the regulatory environment will be impactful in various ways. In some regards a sound regulatory framework could provide them with a clearer landscape in which to operate. Clarity could bring confidence, helping investors decide whether or not to incorporate crypto into their business plans.

We’ve seen a number of traditional finance players begin to dip their toes into crypto waters, and I would expect that more will come over time, under the right circumstances.

All told, I don’t think regulation is an inherently bad thing. I do think that broad mischaracterizations, however, are. In the coming months I hope the focus of legislation focuses on the actors, and not the asset.

Tokenization and the Future of Crypto

By Pedro Palandrani, Director of Research, Global X ETFs

To state the obvious, 2022 was a challenging year for cryptocurrencies. However, in 2023 major structural benefits – such as traditional finance (TradFi) companies still entering the space – are emerging that may support digital assets for years. That extends beyond just crypto’s prospects as an investable asset. Blockchain technology continues to tantalize with features like better security, decentralization, immutability and more. That’s especially clear when it comes to tokenization, or the process of bringing financial and real-world assets onto a blockchain in the form of tokens. And understanding tokenization is key to grasping the long-term investment case for crypto assets.

Despite the crypto bear market, there are signs of life in security tokens. One notable offering was KKR tokenizing part of its Health Care Strategic Growth Fund II (HCSG II) in conjunction with a company called Securitize. But the field is nascent and has a total market cap of only around $90 billion, with $20 billion of that in the secondary market. This is a pittance compared to the hundreds of trillions of dollars stashed globally in real estate and equities.

Tokenized securities have so much room to grow because tokenization creates new on-chain markets for a wide range of nontraditional asset classes. For example, tokens can help create blockchain-based loyalty programs that reward owners with perks for making a certain amount or frequency of purchases. Likewise, membership non-fungible tokens (NFT) can offer rewards such as exclusive features including private events, loyalty perks or early access to new releases. Starbucks, for instance, recently began beta testing Odyssey, a rewards program through which customers can earn NFTs on the Polygon blockchain.

Gaming also has enormous promise. Through a game-and-earn model, tokenization lets players be rewarded with more games and exclusive in-game content. The video game industry generated something like $200 billion in revenue last year, with only about 3% of that tied to game-and-earn. An expansion would be a huge coup for blockchain adoption. Because of this potential, video game projects raised 50% more in venture capital in the first half of 2022 than they did in all of 2021.

It is becoming clear that tokenization has the potential to bring value and liquidity to assets that were previously nontradable. Despite tailwinds in 2022, the creation of on-chain marketplaces for these assets is continuing apace and should support the growth of crypto assets worldwide and the long-term bull case for digital assets broadly.

Takeaways

From CoinDesk's Nick Baker, here's some recent news worth reading:

- SUPERLATIVE INFLOWS: Digital-asset investment products got the biggest inflows in six months ($117 million), according to CoinShares. This is not a gigantic sum in the grand scheme of crypto, which is back around the $1 trillion market capitalization mark. But given how bad 2022 was, it’s something for optimists to latch onto.

- PAY WITH DOGE? The Financial Times reported that Twitter is laying the groundwork for a payments service. Here’s the tantalizing line from the article for the crypto crowd: “[Elon] Musk has said he wants the system to be fiat, first and foremost, but built so that crypto functionality could potentially be added at a later point.” It’s anyone’s guess how Twitter will emerge from its current turmoil, but a Musk-backed crypto payments system would be appealing to some – and could provide a tailwind to efforts to get crypto into mainstream banking and finance.

- BINANCE IN INDIA OR NOT? After FTX’s collapse it became clear Binance was the leader among centralized exchanges in terms of clout. A CoinDesk investigation revealed that Binance has been throwing its weight around behind the scenes as it distances itself from WazirX, the Indian exchange that has been accused of abetting money laundering.

Related news

Three Arrows Capital Founders Launch Exchange Where You Can Trade 3AC Bankruptcy Claims

Bitcoin Miners Surface for Air as Sliding Natural Gas Price Provides Cost Relief

FanDuel Co-Founders Raise $4M for Digital Music Collectible Startup Vault

Bank of America: Innovation to Expand Decentralized Finance Functionality Over Time

Bitcoin Exchange LocalBitcoins to Close, Citing Market Conditions